Forecasting CPI inflation under economic policy and geo-political uncertainties

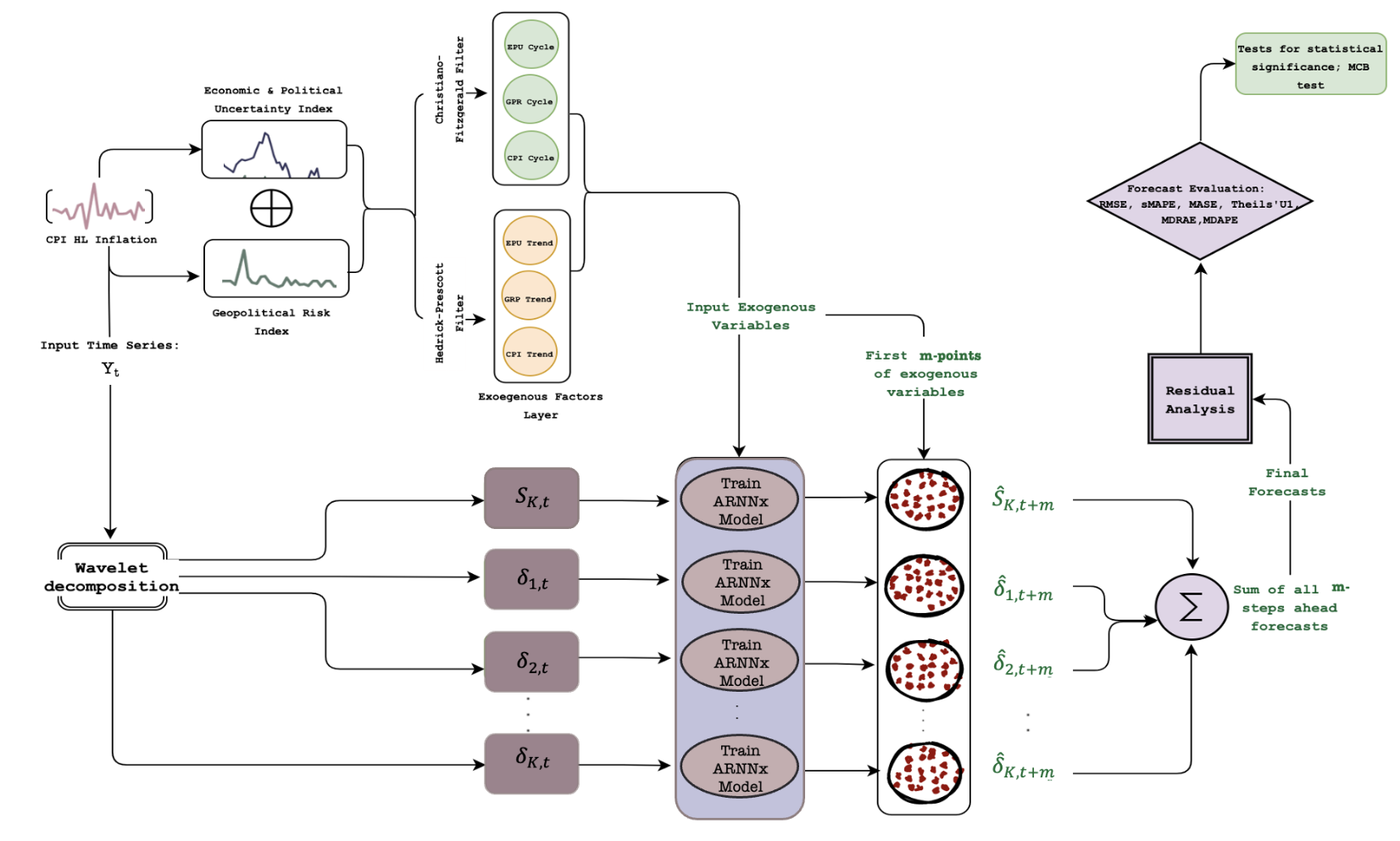

Forecasting a key macroeconomic variable, consumer price index (CPI) inflation, for BRIC countries using economic policy uncertainty and geopolitical risk is a difficult proposition for policymakers at the central banks. This study proposes a novel filtered ensemble wavelet neural network (FEWNet) that can produce reliable long-term forecasts for CPI inflation. The proposal applies a maximum overlapping discrete wavelet transform to the CPI inflation series to obtain high-frequency and low-frequency signals. All the wavelet-transformed series and filtered exogenous variables are fed into downstream autoregressive neural networks to make the final ensemble forecast. Theoretically, we show that FEWNet reduces the empirical risk compared to single, fully connected neural networks. We also demonstrate that the rolling-window real-time forecasts obtained from the proposed algorithm are significantly more accurate than benchmark forecasting methods. Additionally, we use conformal prediction intervals to quantify the uncertainty associated with the forecasts generated by the proposed approach. The excellent performance of FEWNet can be attributed to its capacity to effectively capture non-linearities and long-range dependencies in the data through its adaptable architecture.

PDF Abstract